I came across this idea in a novel I was reading. It requires you to apply compound interest.

Reminder. Express the % by adding it to the 100%. So 5% becomes 105% which becomes a multiplier of 1.05. 5% growth for ten years is then 1.05ⁿ.

Questions

1. Imagine you have an investment at 11% inflation. Imagine this runs for 10 years. Find the result if you had £1000 invested.

2. in 1976 we had inflation at 2% a month all year. What was the inflation for that year?

3. Suppose that inflation rate had continued, at exactly 2% a month. Show that in about three years your money to be worth exactly half as much. [This is the same as asking how many months does it take to reach 200%].

4. If inflation is at 2% a year for a long time, how many years (to the nearest year), will it take to half the value of your money?

5. Repeat the idea in Q4 for 3%

6. Repeat the idea in Q4 for 4%

7 Repeat the idea in Q4 for 6%

8. Repeat the idea in Q4 for 8% and 12%

9. I carefully picked factors of 72. {2,3,4,6,8,9,12,...}. Your integer answers to questions 4 to 8 can be approximated by simply dividing 72 by the inflation figure. Use this approximation to answer this: How many years would it take for 9% inflation to half the buying ability of your money?

10. Is there a similar number to 72 for inflation reaching 300%, i.e. for the buying power of your money to be reduced to a third?

11. Actually, the approximation is better for smaller increases. Find the equivalent to 72 for money to rise to 150% of its current value.

12. Guess the equiavalent approximating number for 250%. You might confirm that you're right, but this is not necessary.

It is not necessary to be able to do logs (logarithms), though it does help. I'm quite happy for you to do (good) guesswork and simply show that your integer answer is close enough.

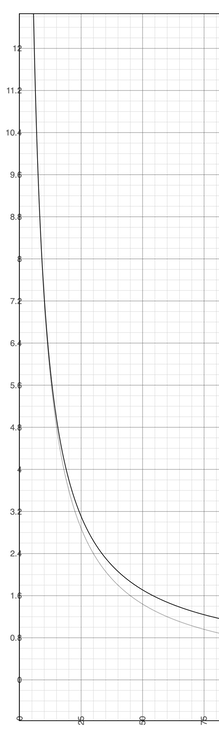

The rule of 72 says that the number of years to double your money (to halve the value of money in inflationary times) you simply divide 72 by the percentage inflation and this will give a pretty good approximation. This is because the y=72/x curve is pretty close to the curve y = (log 2)/log(1+x/100)|, which I have bothered to graph, below. You can see that there is a very good fit for low values of x.

Advanced mathematicians (able Y12 and Y13) might show that the linear expansions equate for sufficiently small values of x. Less able mathematicians look at the curve and say "See, it works".

DJS 20230714

A1. £1000 x 1.11¹⁰ = £10,527 ten and a half times what you began with.

But, if one had 10% inflation for ten years, then what £1000 bought at the start would only buy £95 (£94.99) worth of those goods.

A2. 1.02¹² = 1.268 so 26.8%, 27% to the nearest integer.

A3. 1.02³⁵ = 1.9998896, very close to two. So in 35 months, not quite three years, money has 'grown' to twice what it was, which means that it buys only half of what it did.

A4. Use the last answer; 35 years. 1.02³⁶ = 2.04

A5. 1.03²⁴ = 2.033 (log2)/(lg1.03) = 23.450

A6. 1.04¹⁸ = 2.026 (log2)/(lg1.04) = 17.673

A7. 1.06¹² = 2.012 (log2)/(lg1.06) = 11.896

A8. 1.08⁹ = 1.999 1.12⁶ = 1.974 (log2)/(lg1.08) = 9.006, (log2)/(lg1.12) = 6.116

A9. 72/9 = 8 so eight years. Check: 1.09⁸ = 1.993

A10 Yes, about 112.

A11. I looked at values of (log1.5) /log(1+i/100) e.g. log 1.5 / log 1.05 = 8.31 suggests 40-45. I guess 42 (having several factors) log 1.5 / log 1.03 = 14; log 1.5 / log 1.04 = 10.34; log 1.5 / log 1.06 = 6.95; log 1.5 / log 1.07 = 5.99; This confirms that 42 is a good estimator.

A12 I'd guess at 96 for 250%.Mostly because 96 has lots of factors and is in about the right place. log 2.5 / log 1.03 = 31 suggests 93; log 2.5 / log 1.04 = 23.36 suggests 96; log 2.5 / log 1.06 = 15.72 suggests 6x16=96; log 2.5 / log 1.08 = 11.91 suggests 96; This confirms that 96 is a good estimator.