I am often reading about Generation Rent. Here I test the implication that house ownership is perceived as unaffordable.

My first house, bought about the time I left university, was £7000, of which we (the wife & I) had £2000, one thousand each. Our mortgage was less than four times the higher salary, and double our combined salary. The saved capital constituted around 25% of the purchase price.

A couple embarking on married life in the same way would be earning at least £17k each, since the poverty line is drawn at £16800. So proportionally their mortgage would be £70k and that means that their capital saved would be (again, proportionally) 40%, or £28k and their house would be £98k. Is this reasonable?

Savings of £25-30k means £12-15k each. Is that feasible? I am far from sure, since my capital was my own savings — £500 by the time I left school, plus £300 from university grant, £200 inheritance. Both of my children received a similar amount at current value on their majority (from grand-parents) and neither of us asked the bank of Mum & Dad for capital, though we did ask for loans later, when we started playing games with houses. I think our longest loan, mortgages excluded, was three years.

I made a good deal of my savings from my university grant. A current student might do the same by taking on more loan than needed at university and in effect adding that to the borrowing to be paid off in the far future. Some significant proportion never pay off their student loans.¹ These days I expect that student age people ask their parents for such a sum. "Dad, can I have £10k?" Just like that. And many will be told to get lost. Perhaps the significant difference is that I was saving for the unknown at an early age — I had the saving habit. Sources [6 and 7] tell me that around 80% of under-30s use their parents to buy their first home.

I have discussed this with my daughter and her husband, who both experienced different versions of university fees. The savings equivalent held by my daughter disappeared in reducing the university loan, under the strong perception that any borrowing is bad. As she says, there was little or no incentive to do saving of any description. The perceived imperative was (always) to have the best place that could be afforded. So, when renting, there is necessarily nothing left over to put aside for a future house deposit, because those funds already went into renting a better place. That is a life choice; it implies a decision taken, but I suggest that the issue never quite surfaced to be decided upon.

The daughter went on to tell me that people now marry later than I did, so my model is way wrong. My response is that marrying later leaves longer still to have generated (earned) savings. She also says that many live singly, so that means no pooled income; I recognise this, but suggest that a single person makes different sorts of decisions, even when it comes to owning property.

I quote a remark she made about the son-in-law: He married me when he was 23 and was still the first of his peer group to get married; five years later, none of those peers own their own home, none of them have kids and only one has got married. So I think a lot of the millennials you are talking about are trying to buy a house *on their own*, rather than with a pooled income.

We went on to discuss whether anyone who is working lives within their means. I say this is a life choice, even if an unconscious one. We agree that the savings habit seems to have disappeared. In an environment where inflation is low and interest rates similarly low, there is very little incentive to save and far more to spend. The arguments for renting, indeed for renting anything—like the phone or the car or one's entertainment—are made stronger in that economic environment.

So, let's move on to the position of the first house, where we say the equivalent to what I paid is £100k.

How many houses can you buy for under the £100k? Well, what I bought was a tiny terrace on a busy road in an expensive city, Cambridge. Which is possible in Waterbeach (Cambridge outskirts, a fair cycle ride), just, but probably means you're buying an apartment. I found while writing a new house in Soham (CB7, too far to cycle, say I) for £90k. A new house, not a dilapidated heap in dire need of rescue. So yes, you can find houses under £100k, even in 'nice' bits of Britain (places where your job might be 'nice' too). In Blackpool, there were, at the moment I asked, 1000 properties within 3 miles of the centre of town and 2000 within the same range of central Newcastle. Newcastle has many properties at £90k quite a bit nicer than our second house, which suggests to me that the savings element of my posed problem might be more surmountable than I had expected.

Short version: proportionally, the situation has not changed. So what has changed? The published perception is that the younger generation "cannot' afford to buy, but certainly we can show that far fewer of them are actually buying houses. Source [1] says, c/o the ONS [2], that home ownership in those between 22 and 29 has dropped from 37%in 2008 to 27% in 2018. Further, the proportion with any savings at all went from 59% in 2010 to 47% in 2014. Only the top 10% has more than £15k saved. The same source [1] points to a lack of emotional resilience as a significant factor (meaning they would struggle with a financial shock or income loss). Read the report for yourself at [2], though there isn't much there (suggesting it reflects the ONS opinion of how little a millennial is prepared to read before ditching a site).

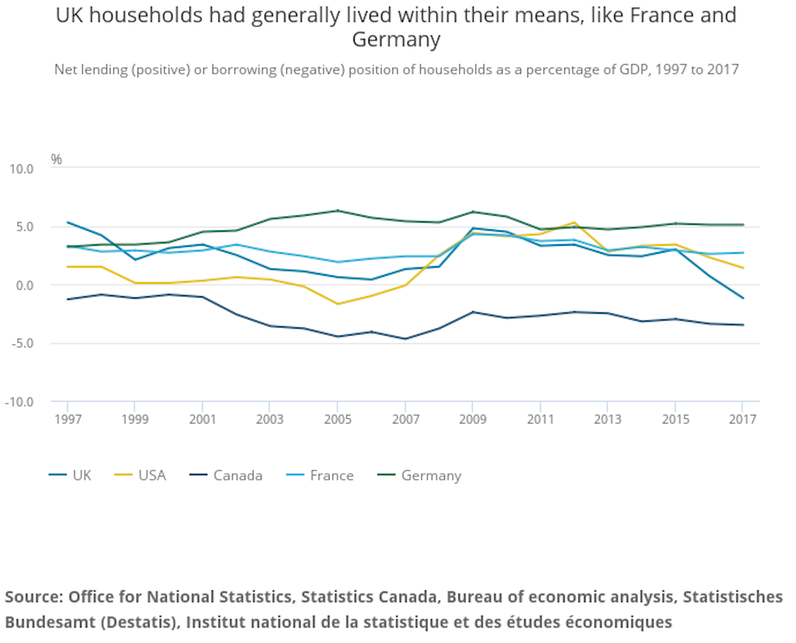

This compares the UK with USA, Canada, France and Germany. The UK line is the one that ends going steeply downwards in 2017. From [3]. Canadians do not have much of a saving habit; the French are good at this. American habits seem to be an exaggeration of ours in Britain.

There's a thing called a LISA, a lifetime ISA, individual savings account, with a ridiculously low take-up rate. You put in up to £4k per year and use it for your first house deposit. It is a really good deal, since the state adds 25% to whatever you save each month. Read about it at [4] and use the links. This is ten times the interest rate you might make on a savings account; I do not understand at all why it isn't in huge demand. The associated personal savings allowance (PSA, for ISAs) allows you to put aside £20k per year and is tax-free (you are not liable for gains under £1000 a year, however unlikely you feel that may be) - but you might do just as well talking to your bank about savings, unless you're doing very well indeed financially. I see ISAs as something for later life, for supplementing the pension fund and so on. I don't think the interest rates on an ISA are high enough to be attractive in terms of gains, but saving is putting money aside first and hoping you can make it grow comes a poor second (until greed licks in, when you'll back more risky ventures including buying a lottery ticket every week). ISAs are surprisingly flexible with regards to taking money out; personally, I have found it far harder to put money (back) in, given the anti-fraud hurdles to jump.

Why would you want to be a house owner? This is debatable and the public is divided. Most of those that own their own house (nominally, the mortgage provider owns more of most houses), disregard the money they spend on their house each year and instead stare avidly at the growth of that value in the market. Reading about this simply demonstrates an abundant lack of decent research. How much do we spend on a house to keep it in exactly the same state as it was at the same moment last year? Few of us admit to even recognising such a thing, but if you were to view this a s servicing your investment without (yet) being taxed on that, you might see this as still being a good deal. Very many of us have our house as by far our biggest investment and are relying heavily on it going upwards in value, even relative to inflation. For a long time this has been true, but do look into what happens when property prices drop. Try looking at the 70s and early 80s for example, and then again 2008-10. It is no worse than the stock market crash, but if you've over-borrowed, you end up with nowhere to live. So don't over-borrow!

On this topic, there is a strong incentive, in my opinion, to take all spare cash and use it to reduce the mortgage. The reduction in interest paid is far higher than the available interest rates on any other saving. The downside, of course, is that you cannot easily change your mind and use those monies for something else. So, funds moved this way need to be labelled as surplus in a way that many may find too difficult. However, the numbers are easily studied and easily understood; this is much the best way to improve your capital standing - that is what you are doing, moving cash into capital.

This distinction between cash and capital may not be appreciated. Think of cash as liquid and capital as solid, and you'll have most of the idea immediately. The way I view things, I have income, most of which disappears in daily running costs such as food and utilities. All of that is cash, liquid money. Relatively little is spent on things like clothes and entertainment, if we bury all the communications costs with utilities. I spend quite a lot maintaining the house, which I think of as servicing that investment, so that might be cash spend or it might be capital spend - the test is probably "Does this add value to the house?" If yes, it was capital spend or cash moved to capital, and if not it was cash spending.

The next significant spend is depreciation - I run a car and several computers and I plan to replace these eventually, so I should have put aside the funds for that. And, you say at this point, "Dream on" and "Get real". But I have the advantage of years of doing this and I've learned the hard way that I must do this accounting, even if all I do is recognise that this year I don't have funds to cover depreciation. But this depreciation thing is not cash, it is capital. If capital is somehow 'solid' money, this is erosion. Most of my capital goes up in value (house, particularly, investments occasionally), but the car and the computers go down in value. So either I 'pay' for this depreciation with capital somehow, or I try to cover it with income.

By this point, many readers will be saying negative things and thinking they never reach such a moment. Yes you do, but there are two factors preventing you from recognising the moment: one is simple to recognise - the cash spent adds value to some capital item - but this is difficult to express in the household accounts; the other is that so many people simply don't make any attempt to do domestic accounting. I've kept accounts since before I left home, so I have always been easily aware where my money was going to (and I'm a miser at heart). As a retired person, what the capital does is important but in a different way to the position of 40-50 years earlier, in that income is expected to hold steady or decrease, where before it was always expected to increase. So the capital must work and be seen to work – indeed, there is more to be gained by studying what one might do with capital.

I wonder if there is also a change in what is acceptable as housing. Several of the young people with whom I communicate seem to expect that their house will somehow always be in good condition, desirable etc. Perhaps that also indicates a lack of make-and-mend skills, and perhaps an unwillingness to learn such skills or even a tendency to do a lot of living outside the nest. That would be very difficult to measure, but I did find a load of references to younger generations presuming upon their parents for repair and maintenance; that may be an indicator of other trends in society of acceptable industry too. What I'm saying here is that expectations may (also) have changed from when I began house ownership, or that I was already falling outside the norms of behaviour. I think my conclusion almost fifty years later is that if you want to own property you need to work at it and work on it, which means living in less than optimum conditions while you do that work - indeed, for that to be the norm, because each time a house is 'finished' it is time to move onwards and upwards.

The daughter went to apply for a mortgage. She took with her the domestic accounts and a spreadsheet that showed what their upper limit on borrowing would be. Of course she did. That figure had little relationship with the upper bound on what the lender might proffer, and I have done this myself several times in the past. My brother donates time to Citizen's Advice; he says he has quite a few customers (they're called clients) who have a very good grasp of their money traffic, but that most have very little idea at all – from the way he's talked about this I understand it is a U shaped distribution, few people in the middle. Meanwhile, the daughter said the mortgage broker's reaction was that she'd never seen such a thing, someone so organised. The daughter's response in turn, predictably, was to wonder how one could function without such preparation. Of course, I agree with her. Not least because she's a scary person to argue with.

So the proposition is that the situation vis-a-vis buying a property is not all that different from when I first did it. One still must wait until earnings are large enough to afford something else (in some sense 'better'). One still has difficulty 'getting onto the property ladder' and that still largely means putting upon the older generation for a significant leg up. Which, even when it does happen, may well mean living somewhere a good deal further down the ladder than earlier perception suggested would be acceptable. What has definitely changed is a number of perceptions about this general situation, which I begin to think centres around the changes in the way we now pay for tertiary education.

As an aside of sorts, let's look at the choice between renting and owning. What are the benefits ? Mobility, mostly. Lack of maintenance for many – but of course, you're paying for that privilege. Try [5] for reasons and look at {12].

There are two pairings of factors we can point to: parents did not pay for university and their kids are doing that (or will); so in a sense Mum and Dad have money that a previous generation had already spent and, though far fewer of the earlier generations went to university, we might recognise there was probably a similar pay-out for career training of one sort or another. So I think those two factors are intertwined.

The other pairing is a change in expectation of the immediacy in reaching a goal, such as 'having a nice house'. Mixed with that is a number of changes socially in the transience of any given situation – renting instead of owning is both a symptom and a cause here. If one rents the best one can afford, there will be no saving for future ownership and it is likely that the saving habit was never acquired. People that own houses have different aspirations – or, perhaps they have the same aspirations expressed differently. There is a sense in which ownership of anything is no longer a desirable; the 'freedom from clutter' meme has taken root and that has turned into an intention to stay clutter free, responsibility free, free of ownership of property and its attached responsibilities.

Do not assume that other countries hold house ownership in the same regard as in England. 2007 73% to 2016 63% sounds awful when described in [8] but so many of the necessary numbers are hidden. This is selective reporting and the Independent is usually better than that (or I hope it is). Scotland: 1981 40% owner-occupied, 2000 63%, 2015 58%. That 1981 figure was already a large rise on the 1970 figures, not shared by [9]. ² Poland is up to 83% (2104), France 65% (2014). Compare figures at [10].

Such dramatic differences across only Europe tell us quite a lot about attitudes. Quite clearly we have a sea change in Britain, away from ownership. So who is paying for this? What is actually being bought when one rents? How is any semblance of standard maintained – and how might any party involved, from the renter to their politicians, do anything to cause standards to improve rather than decline? At the moment we don't have the funds to police housing, since that is a council task and currently so far underfunded I cannot see any council fulfilling but a fraction of their expected duties, presumably at the more desperate end of the scale. Does this, in turn, mean that we are allowing a downward slide to occur, or simply ignoring it until it 'matters' enough to overtake other issues? Are we, yet again, going to blame Brexit for this? Of course, it is the causes of Brexit that this situation illustrates, not the event itself. Austerity may or may not have been necessary, but this is one of the knock-on effects. The question has to be 'Who pays?", but behind that there are more difficult questions about assumptions of responsibility. ³

I suspect that it is the issue of responsibility that underlies much of this. It may indeed be that the cries of 'nanny state' are coming back to bite us, in the sense that, however much any or all of us have complained at the perception of the nanny state, we have, quite possibly all slipped towards acceptance of that. In so doing it is likely that we surrendered some part of our own responsibility—for ourselves—as some might argue takes place when one chooses to do nothing about saving. One might equally argue that learning about fiscal responsibility is and was someone else's responsibility. It was; it was your parents' task, just as it was your own to do thinking about your life position and what you might do to better it. If you chose to do none of that thinking, even from ignorance, it is, I'm afraid, your responsibility. An uncomfortable truth. "Why did nobody tell me?" I hear; I might just as well ask "Why did nobody listen?" I taught about such things often enough in lessons for there to be complaints – I am unrepentant and as unrepentant now as then; maths needs to be seen to have use, and the only lessons in which it is acceptable to talk about the uses of numbers (the uses to which numbers can be put) is those many maths lessons. It is also only Maths or English that has so many lessons (typically every day) that such comment can readily be made.

I wonder also if there is a change in the way we view employment. Tony Blair told us all to expect to have four careers and therefore we needed to accept the idea of lifelong education. I thought this entirely obvious at the time but recognised that not only did it need to be said publicly and often, but that we all should be planning to cater for such life changes. Which is not quite the same as waiting until such change is visited upon us, more a case of being responsible enough and responsive enough to be able to cope with such a magnitude of change. As, indeed, many of us will be discovering in the next two years as Brexit bites properly. Even if there is a reversal of the exit itself, I expect that we will still have significant ructions in the economy and not merely transitory ones. Brexit is not the only reason for dramatic economic change, but that is a different issue to discuss.

I see a social swing towards us being required to take (more) responsibility for ourselves. One such is to be seen in the NHS, which has to move from healthcare —caring about a lack of health— to the health of the nation as a whole. To make that happen we must be persuaded to be (far more) responsible for our own health. I expect this to be paralleled in many other spheres. It is clear to me that we are each able to be responsible for ourselves and that we should not be relying upon others to do our thinking for us, to take actions on our behalf. Of course, we should be grateful if such events occur, but we should, in my view, be aware of having mostly avoided needing to be helped. Stand up for yourself, not in terms of demanding that others act for you, but in the sense that you deal with your own problems in a positive way. Take charge of your life.

As I have written before on these pages, Mother had a phrase that covered every occasion when you identified a problem, now known as Barbara's Question:

What are you going to do about it?

DJS 20190218

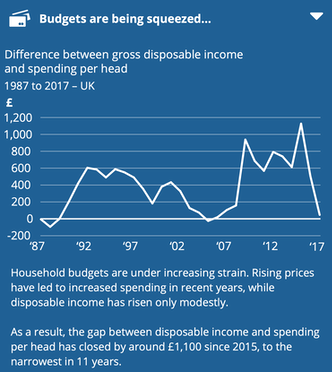

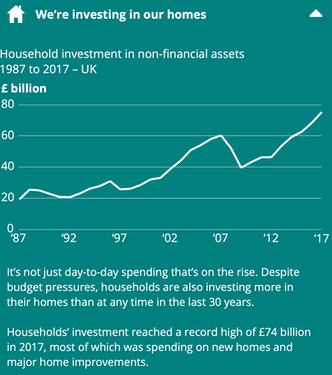

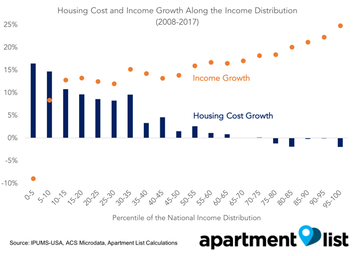

top pic: both the blue and the green inset charts are from sour [2], the ONS.

Thanks expressed here to Jessie for her contributions and for persuading me into a more constructive approach.

[4] https://www.moneysavingexpert.com/savings/lifetime-isas/

[5] https://www.moneyadviceservice.org.uk/en/articles/should-you-rent-or-buy

[6] https://www.bbc.co.uk/news/business-39778029

[9] https://www.gov.scot/publications/housing-statistics-scotland-2017-key-trends-summary/pages/6/

[10] https://en.wikipedia.org/wiki/List_of_countries_by_home_ownership_rate

[11] http://www.scotlandhousingcrisis.org.uk/scotlands_housing_crisis/

[12] https://www.zoopla.co.uk/discover/renting/rent-or-buy/#vz4dp0cUGsxH5X6O.97 A discussion of this same topic from the standpoint of an interested agent.

[13] https://www.citylab.com/equity/2019/05/affordable-housing-rental-income-inequality-data-homeowners/588109/?utm_campaign=citylab-daily-newsletter&utm_medium=email&silverid=%25%25RECIPIENT_ID%25%25&utm_source=newsletter This doesn't entirely agree. perhaps suggesting that there is a change on the way, already visible in the USA. City Lab explores this sort of thing all the time, but concentrates on US positions. Despite that, I find it helpful in the sense that at least there is someone writing and attempting to think about such matters. Enter the phrase rent-burdened, which is when 30% of earnings goes on housing. I'd like to compare that with UK figures. The US situation is different, for many more have mortgages - and for longer, into later life. Note, too, an apparent difference in disposable income between renters and owners: the renters show a greater growth in income (not more, growing faster); an apparent consequence is that more income goes on housing (rent). This is especially true at the lower end of the spectrum, which may be a hangover from the 2008 crash.Or, to put that another way from the same figures, rent has gone up fastest at the low end of the spectrum - this is widening the inequality. We moan in Britain, but too often the situation in the US for a topic is worse still. Essay topic for you (not me).

1 The Institute for Fiscal Studies estimates that around 83% of graduates will have some debt written off under the current system. So around 17% are expected to repay in full. https://fullfact.org/education/about-17-students-are-forecast-fully-pay-back-their-loans/ The latest estimate from the IFS is that the taxpayer may end up paying for around 45% of the loans of students starting in 2017. The increase in the earnings threshold pushed this up from about 31%.

2 from [8] The UK has experienced the largest fall in home ownership of any country in the EU since the financial crisis.

The proportion of people owning their own home collapsed 9.9 percentage points from 73.3 per cent in 2007 to 63.4 per cent in 2016. That compares to France which has seen a rise in home ownership of almost 5 percentage points in that time, data compiled by Bloomberg Economics shows. Poland registered the biggest increase of more than 20 percentage points.

The research is the latest to underline the reality of the housing crisis in the UK, putting fresh onus on the main political parties to demonstrate how they will fix the problem which has disproportionately affected people aged under 40.

Among those born in the late 1970s, 43 per cent owned their home by the age of 27, a figure that dropped to 33 per cent among those born five years later and 25 per cent for people born in the late 1980s, a recent study by the Institute for Fiscal Studies (IFS) found.

Scotland 2011, 62.5% owner-occupied, remainder rented. [10] 1981 council house (rent) was 55% [11]. It would be wrong to assume such figures are evenly distributed; in 1978 I was told that Glasgow was 90:10 renting over owning (by both the universities of Edinburgh and Glasgow), while at the same time the figure in England was 20:80. I entirely failed to find evidence now for that assertion, so maybe it was so widely accepted no-one bothered to test the figure. Access to information is far easier now, though I have no doubt that proving an assertion correct is no more difficult. Fake news, etc, etc.

Similarly in France the 65% owner occupied rate implies 35% renting. Renting is far more likely in Paris; I think I read an implied 80% renting figure. The high figure of 83% owner-occupation for Poland needs to recognise the dramatic change from 65% in 2007, as implied in the quote above.

3 By some coincidence or synergy, one of the royal couples came to Blackpool this Wednesday (20190306) and spent some time looking at rented accommodation here. They were shown some truly awful places and were quite clearly moved by what they were shown. The sort of places where the condition was so poor that rent seems an inappropriate concept. Appalling landlords? An expression of the desperation in the market that such places can be rented? Failure of building control? All of the above? Yes, we need action, but to do that we need better regulation and support of those regulations, which probably means funding. I do not personally feel it is my duty to pay for this locally in council tax, but I accept that this reaction is because I already pay the most in our immediate location, so the burden of additional council tax will fall on me, which I resent. It is bad enough that I have to spend over the odds because we live in a conservation area..... rant, rant; my choices, my consequences, my problem.