Among the shouting and screaming about the unfairness of the tax hikes in National Insurance were a number of calls for a wealth tax. I hope to look at what form these might take, while reviewing who is hit by the current ideas for taxation.

In principle a wealth tax applies to individuals real and corporate. Wealth includes the total value of personal assets, including cash, bank deposits, real estate, assets in insurance and pension plans, ownership of unincorporated businesses, financial securities, and personal trusts (a one-off levy on wealth is a capital levy). Since one deducts liabilities such as mortgages, this might properly be called a net wealth tax. Quite a few countries have this sort of tax. ¹

From the foreword to [2] This report will not change everyone’s mind, but I welcome it as an important contribution to the debate. It has been led by a team with the essential mix of skills in economics, tax law and administration, who approached the subject with an open mind. They conclude that an annual wealth tax is a non-starter in the UK and we should fix our existing taxes on wealth instead. However, a one-off wealth tax is a very different proposition.

There is an underlying assumption that economic inequality is increasing. ²

The UK already has taxes on the transfer of wealth; Capital gains tax (CGT) taxes the increase in value of items of wealth; council tax is based on property values (though in 1991) irrespective of liabilities such as mortgage or lessees. There are other wealth taxes and I think inheritance tax belongs in this group, as does tax on investment income.

A one-off wealth tax payable on all individual wealth above £500,000 and charged at 1% a year for five years would raise £260 billion; at a threshold of £2 million it would raise £80 billion.

One-off wealth tax There are positive attitudes to a wealth tax, but I suspect that is because a majority think it will hit 'the rich' and not themselves. For those hit hardest (so says the press) by direct and non-regressive taxes, this is undoubtedly true and in terms of balance, that makes a tax perceived as top-heavy quite attractive. A wealth tax [2, p5] should be fair, efficient, substantial (it raises a lot), difficult to avoid and, says the summary, it should achieve all of these better than the alternatives.

The one-off wealth tax levied at 1% above £500,000 would require a couple to have net wealth of more than £1 million before any wealth tax would be payable. Alternative tax rises which could also raise £250 billion over five years include: Basic rate of income tax to rise by 9p (20p to 29p); All income tax rates to rise by more than 6p; All VAT rates to rise by 6p (taking main rate from 20p to 26p); Corporation tax to rise by 5p and VAT to rise by 4p. [2, p5]

Have we had one-off taxes before? Yes, 1981 under Mrs T there was a windfall tax on banks and 1997 under Tony Blair a windfall tax on privatised utilities. Note there is a reliance on people being unable to respond before the tax is introduced. Thus a feature of such a proposed tax is that it applies from the moment of it being passed, or even earlier, such as the end of the previous fiscal year.

The report (that I'm helping you avoid reading) describes several design conclusions, which I include below.

• Wealth tax in levied on an individual, not a household. Yes, joint property is a shared asset, but this is consistent with personal taxation. Ideally, as with income tax, you could choose to be taxed as a couple or as a pair of individuals.

• wealth tax should include all the property of an individual. That is, if you hold cash and I hold property, we should be taxed in a similar way. Pensions are definitely assets in this regard. Tax specialists give this funny labels such as sideways equivalence; the point is that people with equivalent positions should be taxed equivalently. If you were thinking of that cash vs property issue, imagine yourself in that transition between houses where you are temporarily (very) cash rich and without the house asset.

• Assets are based on their open market value. That puts lots of work on the several valuation offices. The share businesses do this all the time. A smart politician will want to make this someone else's problem, but it cannot be the owner's problem, since it is their interest to have the lowest believable valuation. So it has to be an inspectorate of some sort, with loads of capacity for problem resolution. Which, like council tax, really means complaint.

• People who are asset rich but cash poor can defer (perhaps until death); such a tax should not require sale of the family home to pay a relatively small amount of tax. The numbers are known; when the threshold is £1m per couple, 570,000 are liquidity constrained, while at four times that, only 65,000 have a known problem. Such a tax should not create hardship. But then neither should end-of-life care. I see this as an issue for the politicians to (re)solve. The idea of a one-off tax proposes a 1% tax paid across five years; those with liquidity issues need attention and assistance and ways for deferral to occur; there may well be opportunities here for private endeavour. The tax cannot be waived, but a lien on the property might well be one route forwards.

Annual wealth tax The serious drawback with this idea is the need to assess wealth frequently. It would be much easier to reform other taxes on wealth. However, if the aim was to change the distribution of wealth and so reduce inequality, the thinking might change enough to explore this idea more fully.

The drawbacks to an annual such tax are (i) significant administrative costs attached to frequent asset calculations, even if the threshold is set quite high – which of course reduces the revenue raised. (ii) Those liquidity concerns raised above could quite easily limit the rate that can be set; since the tax is annual, deferring tax will not work and in effect this pushes assets towards breakdown. Perhaps one would simply sell large properties to the National Trust or equivalent, and assume that such a body would be exempt. (iii) It would not take long for the tax to be avoided, in the sense that behaviour would change in response to the tax. As the report says on p8, the evidence from other countries attempting this is that 7-17% of the tax base would be lost, even with a low tax rate of 1%. (iv) Any exclusions or exception cause a change of behaviour, to move assets into the excluded or excused classifications. You might call this tax avoidance, but from a revenue perspective it is lost monies, though we can easily argue that the change in behaviour is caused by the taxation, itself a disincentive. (v) as the tax becomes understood, so high thresholds cause long-term behavioural change, such as holding property in many names so as to reduce (wealth) tax liability – in effect to spread the wealth around within the family group so as to prevent it being spread across the whole nation. An understandable behaviour. The very rich would simply leave.

Do read the summary report to understand the detail here, pp8-9.

At the foot of the summary are some observation worth inclusion here. One such is that the analysis of who has what is surprisingly poor and so that, for there to be any change in taxes on wealth, we need (very) much better information. Put bluntly, there are many rich people not included in the analyses and surveys. A second problem is the ability of HMRC to deliver a system for a wealth tax. The speed with which the furlough scheme was created and applied shows that HMRC can move quickly, but that this can be expensive and makes for problems. Among other issues, there is no record of the value of individual properties; that not only makes a wealth tax harder to create but it also means that reforming council tax is stymied before it can begin. In effect, the lack of records mean that all sorts of reform are made very much more difficult.

“So is a wealth tax the answer? It’s appealing in theory, of course, but the ‘broadest shoulders’ already bear the brunt of our tax system. The top 1 per cent already pay 28 per cent of the UK’s income tax bill. It’s also the case that a ‘surprise’ tax wouldn’t do much for the UK’s long-earned reputation for a stable and predictable business environment.

“Far more radical would be for the Chancellor to take advantage of the Covid-19 crisis for a genuinely radical shake-up of the tax system that made Britain more competitive. Using low-interest rates now to stimulate growth that can pay to service the debt if those interest rates go up is the path I’d look for.”

Andy Silvester, Acting Editor City A.M.

This last may well be enough to force change in the whole model of what shape a wealth tax might take. Just imagine what would happen if we had a wealth tax but property was excluded. Suppose the only exclusion was occupied housing; that plays into the hands of all sorts of landlords (good and bad), it causes people to want to move other assets into land, thus it rockets the price of housing and rapidly it makes the problems it was supposed to be addressing —redistribution of wealth— an absolute nonsense. What we need is for the threshold to function very well. Suppose the threshold was drawn at the two million mark, £4m for a couple with all assets included; that is 626,000 people and raises 9-10 £bn at 0.57% [Table 8, full report, p84], with 7% of these people being liquidity constrained. Thus a 1% tax here would raise £17bn but more would be constrained A threshold of £1m per individual hits 3 million people, a far higher number are cash-strapped but the 1% level raises £56bn before studying deferrals.

I have no comprehension how or if wealth tax applies to legal bodies that are not people. I am very unclear how we tax (or do not) people who live abroad but hold assets within the UK, but I imagine there is a residence test for any given tax year. See Full, p46. I can see that there would be issues with things such as trust funds, or recent migrants in either direction. I can see that owning a business is an asset, but taxing it as wealth might well put it out of business overnight. Likely exemptions seem to me to include artwork, antiques, heritage and farming assets. One might need to read the 1974 Green Paper too. Labour was elected (1974-6) to provide a wealth tax but left office without that done. [3] ³

What are the existing taxes on wealth? Council tax, inheritance tax, stamp duty, capital gains tax.

As I've written before, council tax is levied on housing based on 1991 prices.⁴ I think that band A rates are close to beoing at-cost, while all the other bands generate money for councils to spend. By cost here I mean the services brought to the door, such as waste removal. Proportionally then, council tax places a greater burden on younger and poorer households relative to older and richer households, and on households in less prosperous regions compared to more affluent areas. Council tax also encourages people to buy and remain in larger homes (Evans 2009). There is a council tax relief system but take-up is around 65%. I have no idea if that is typical or unusual, good or bad. This system could be updated and improved; two-thirds of all properties are in the bottom three bands while everything above £320k in 1991 is in the same band. The system of discounts in council tax also encourages the inefficient use of properties. Discounts of 25 per cent are available for households containing only one adult or 50 per cent for those with no qualifying adult. Councils are also able to give discounts of between 10 and 50 per cent for second homes, while homes that are empty for up to six months attract no council tax. Councils may offer a discount of up to 50 per cent for homes that are empty for longer. [6].

There are two components to council tax; services received, which we could call housing consumption, and another component that funds the everything else that the council attempts to achieve. It can quite easily be argued that council tax is unfair on the disadvantaged and that it adds to the advantages enjoyed by the relatively well-off. The system could well be revised without requiring any increase in total revenue, which I see as a different, separable, argument.

Council tax could be revised into many more bands at the top and bottom with correction from the 1991 valuation. Council tax could be replaced with a housing consumption tax levied on both owners and tenants. 0.6% would raise a sum similar to council tax (and for me personally would be about the same charge). Council tax could be replaced in whole or in part by a property tax (levied on the true owner, not the occupier). See [6, pp14-5].

Some of these changes would be directed at improved fairness. Others are directed at lowering property values, at reducing the incentives to own a house as an investment and (strong approval from me) to discourage leaving any property empty.

Stamp duty, SDLT, is a straightforward tax on the purchaser of property or land. Taxes are set in bands, ⁵ which encourages activity around the thresholds. Detractors say this is a charge on moving house (quite true) and therefore a disincentive (I do not agree, it is just another cost to factor in, like the fees). From the revenue perspective they are easy to collect and hard to avoid. Additionally they reduce the volatility in the housing market, which is probably a good thing. The relaxation of stamp duty during the pandemic certainly stimulated the market. SDLT returns at the end of Sept '21.

Inheritance tax is charged on the estate and to an extent on gifts/trusts in the (six years) period before death. Once the threshold is crossed, it sits at 40%. Spouses are relieved of tax until their (later) demise; farming and business assets are applicable for relief, often at 100%. In 2010–11, a total of 16,000 estates (representing three per cent of all deaths) paid inheritance tax. The number of estates on which the tax is levied, and aggregate revenues, fell significantly after the change to inheritance tax rules for married and civil partnership couples in 2007. In 2006–07, 34,000 estates were liable for inheritance tax. Since its introduction in 1986, the threshold for inheritance tax has more than kept pace with real house prices and has become much more generous for couples relative to average house prices after the 2007 reforms.

Source [6] concludes that housing is particularly undertaxed as an investment in the UK on average, although it is probably undertaxed as a consumption good because no VAT is charged on the construction of new homes (OECD 2011). You can argue that the planning system acts as a tax on housing. ([6] Evans 2009). Consistent comment is that a tax designed to be levied on the wealthy is not fair or efficient if it can be routinely avoided by the very wealthy. I attach to this all sorts of other false values and attributions; it fits all too well the perception that the Conservatives pander to their cronies by making it possible for the very rich to act like this.

Capital gains tax is a tax on profit made in assets, including gifts received. It is not payable on primary residences, but it is on second (plus) homes and on buy-to-let property. It is charged at 10 or 20% depending on your tax band. It is charged on investments including shares, so those who made huge sums on Bitcoin are liable for CGT when they convert bitcoin back to fiat currency. (Check). You have an annual exempt amount of gain, £12300. CGT raised about £9.1bn in the 2019/20 tax year, source.

Note please that [8] says The main wealth and property taxes - stamp duties, inheritance tax and capital gains tax - together account for less than three percent of total revenues. (Council tax accounts for another 4 percent of revenues, but is only a “wealth tax” in the crudest sense of the term.)

It is clear to me that we have a need for improved taxation, just as we have a need to find ways to pay for what was spent during the pandemic. We need a significant increase in funding for health and care, we have deprived many systems of funding (the justice system is one such) and we have allowed this to occur systematically. Conservative governments particularly pride themselves on being for low taxation, but that ends up starving the state of the funds it needs to provide for its people. The desperate need for levelling-up underlines this result of austerity – it has hit hardest the very people it should have been protecting. The Tory cynic says this is untrue, it has only hit the Labour voter. To me that serves to divide which is no help at all and suggests no progress is likely while power is held the way that it appears to be.

I suggest that we have great need for significant change in taxation such that the government can indeed bring about wholesale and necessary change. The climate crisis is a large issue that also demands attention, though I suspect that this will be more easily self-funding. It seems to me that in many ways our taxation system works to keep the disadvantaged in their place (how very Victorian) while simultaneously discouraging effort to improve one's station in life. Instead the system works to preserve the status quo. It would be better if the bottom boundary came upwards and the top boundary came downwards.

Clearly any tax that hits someone else, especially those labelled as 'rich', will be popular. The message received it that there will be money available—and the perception will be, 'to be spent on us'—at no further cost to the many. Working against that are all the vested interests that want their advantage to continue. Selling the idea of a wealth tax is a political challenge, but that is exactly what politicians are there to do. Not the lining of their own nests that we see all too often. What disturbs me is that the status quo is the default position, that politicians will always kick the proverbial can down the road if at all possible, that the political perception is that everything can be put off until it goes away. But climate change and inequality in a rich country such as Britain—the need for levelling-up, as we currently call this—are both immediate matters demanding serious attention and massive spending.

We need statesmen and what we have is populists. We need a system that includes people and we are drifting rapidly the other way. One can hope that we drift enough that enough of us recognise the solution when it is offered. I am suggesting that the time is ripe for a leader to emerge. Even from the inside of Boris.

DJS 20210917

Top pic from [7]

1 France, for example, taxes land property only above a certain large value. Norway taxes net assets including 25% of a first house and 90% of a second. Some countries target overseas assets particularly. One can understand this.

2 ... economic inequality is increasing and proposes wealth taxes as a countermeasure. [2] and here. The contention is that inequality is not an accident, but rather a feature of capitalism, and can only be reversed through state interventionism.[17] Thus it is argued that unless capitalism is reformed, the very democratic order will be threatened.[17] [17] is Ryan Cooper (March 25, 2014). "Why everyone is talking about Thomas Piketty's Capital in the Twenty-First Century". The Week.

3 Interesting times. Elections 1970, 1974, 1974, 1979. Prime ministers: Wilson 64-70, Heath 70-74, Wilson 74-6, Callaghan 76-9, Thatcher 79-90. Change of PM in April 1976 (read). Perhaps it was the change of PM that caused the wealth tax to be dropped. I suspect that it became simply too difficult, having been available for attack since the previous declaration of manifesto, 1974.

4 It is different in Wales, 2003 prices.

5 Note to self; this house is in Band E. The top band is H.

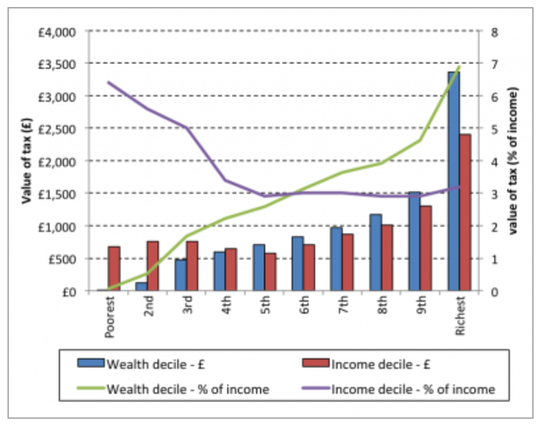

The x-axis indicates deciles. The left y-axis refers to annual council tax (I agree, this is not obvious) and the right-hand y-axis (also confusing) represents % of annual income. So the green line indicates a progressive tax while the purple one indictes a regressive tax.

The red bars show the distributional impact according to income decile (with households in WAS (the wealth and assets survey) divided in to ten equally sized groups according to disposable income, adjusted for household size). The poorest six deciles pay around the same on average in cash terms – between £600 and £800 per year, with higher average cash payments for the richest four deciles. As a percentage of income by income decile (the purple line) this means that the property tax is regressive – the poorest four deciles pay a larger percentage of their annual incomes (on average) than do the richest six deciles. This finding reflects the presence of ‘asset-rich, income-poor’ households towards the bottom of the income scale, which would be an important consideration in any reform plans. However, this regressivity is also present in the current council tax system, but on a larger scale.

The red bars show the distributional impact according to income decile (with households in WAS divided in to ten equally sized groups according to disposable income, adjusted for household size). The poorest six deciles pay around the same on average in cash terms – between £600 and £800 per year, with higher average cash payments for the richest four deciles. As a percentage of income by income decile (the purple line) this means that the property tax is regressive – the poorest four deciles pay a larger percentage of their annual incomes (on average) than do the richest six deciles. This finding reflects the presence of ‘asset-rich, income-poor’ households towards the bottom of the income scale, which would be an important consideration in any reform plans. However, this regressivity is also present in the current council tax system, but on a larger scale.

[1] https://en.wikipedia.org/wiki/Wealth_tax

Summary https://www.wealthandpolicy.com/wp/WealthTaxFinalReport_ExecSummary.pdf

Final Report https://www.wealthandpolicy.com/wp/WealthTaxFinalReport.pdf

An interesting read. Would make the basis of a good History/Politics essay. The font size varies within a paragraph, as if scanned.

[4] https://www.jstor.org/stable/40911162

[5] https://www.cityam.com/a-wealth-tax-could-raise-as-much-as-55bn-but-is-it-really-the-answer/ A short list of scenarios is studied.

[7] https://www.opendemocracy.net/en/opendemocracyuk/time-is-now-for-wealth-taxes-in-britain/