While I remain one who prefers to be a European I accept that we may well end up outside. This piece attempts to discern what we might realistically end up with and without.

I am not at all the first to attempt such a balance, so I will try to lean in the opposite direction from my preference and tackle the question more in seeking what good is to be had in leaving.

In 2016, Britain paid in £13.1bn, but it also received £4.5bn worth of spending, said Full Fact, “so the UK’s net contribution was £8.5bn”. [1]. Mrs May's deal reveals a demand from the EU for £B 39 or so, amounting to at the best a 3-year exit cost, but possibly five. We have figures being thrown around about spend since 2016 on Brexit preparation, but the cost of inaction in so many other spheres of activity is, I suggest, largely unknowable.

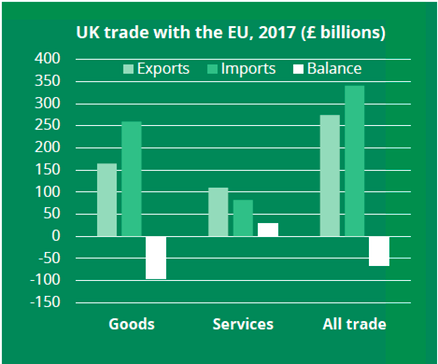

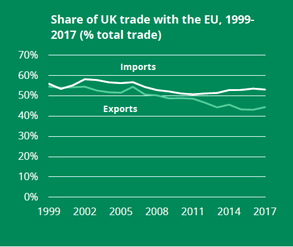

The EU is our largest trading partner, [2, 2017 figures] £B 274 out, £B 341 in, that 's 44% of exports and 53% of imports. Overall then we have a deficit of £B 67 in 2017. We should distinguish between goods and services 1 Surplus £B 28 in services, £B 42 deficit in goods. We still export more goods than services, but the proportion has been steadily falling, at a little less than !% a year, while service exports have stayed at 40%. In reverse, goods imports have been steady and service imports have fallen. See page 8 of the full report at [2]

Will the EU continue to be our largest trading partner? That's crystal-ball stuff, largely pointless. Our manufacturing has shrunk but that could be described as either a set of decisions made at state level, or as the conditions being favourable for providing services instead or, almost as easily, we can point fingers elsewhere and say it is their fault. Why do we make few cars but buy many from Germany? What conditions make that attractive to them but not for us? Are we so very different? I think we made choices quite as much as the EU making conditions attractive for certain activities to be in certain locations. Changing that requires recognition of effects at Europe state level and agreement what we (Europe) wants to do about that - it might be that we collectively decide that cars should be German, not French or Italian. It would be appreciably better for that sort of manufacture to be spread across the continent. This is merely an example, of course. One observes that several Asian tigers deliver large volumes, cars included, to Europe at attractive prices, suggesting that the additional load of form-filling is not insurmountable and not preventing trade.

Britain has turned itself into a banking centre and when we think about 'services' many of us think of the City and all it stands for but I notice again that we still account for more goods than services, which runs counter to the impression left by our press, perhaps due to it being London-centric. It seems already that most of those EU functions that were UK-based have left and with them a growing number of service centres. But, as essay 259 pointed out, that may prove to be a good thing in the long run. I also point out that what we record as import and export does not automatically agree with the figures produced by the other party to the trade; this is discussed in a footnote to essay 260.

When people talk about tariffs there is scope for confusion. The EU sets external tariffs for trade with non-EU countries and there are no internal tariffs for trade within the EU. There is scope to adjust these tariffs on leaving the EU; such decision are political – and so not something for which one can predict behaviour.

DJS 20190400. This is not yet finished, even though it appears to have come to a natural end. I am waiting for finding more to say. Meanwhile, parliament has sent the PM to beg for a longer extension and the result appears to be that we will be having MEP elections despite declaring a continued intention to Leave. This is now considered normal behaviour; we are now that dysfunctional as a nation. Whether we leave or not is still up in the air. Parliament has no agreement worth recording, only extreme differences of disagreement. A number of indicative votes only gave illustration of those levels of disagreement. I continue to see a second referendum (with Remain one option) as the obvious way out of this impasse only if the result is strongly one way or the other; we need to agree in advance what margin declares an actionable decision or that the result is indeed only advisory. Instead we have fallen into a limbo where are neither in nor out, not quite included nor excluded. This may be the state in which we wish to be, in which case I see little appreciable change by reverting to the 'within Europe' as we were before 2016. Politically, both major parties are divided, the Conservatives more so than Labour. In direct consequence we have a proliferation of alternative Leave or Remain parties, but the FPTP voting system will do them poor service unless they are to unite in ways that offer just a single candidate for each constituency. While they are at least as divided as the two major parties they will garner far too few votes to have any effect. I say this irrespective of whether the election is for MPs or MEPs. And I'm assuming that there is a reasonable turnout at any such election, when there is good reason for people to simply not bother, since quite clearly the expression of an opinion does not result in action - which I think is the translation into action or inaction of the squabbling and indecision of our elected members. It is also the root problem with FPTP - most votes result in that individual feeling their vote did not count toward the result.

20210115 Now we're out and there is spome sort of agreement with the EU, the Deal. We wait to discover just what that actually means in terms of what we can or cannot do, and what really changes for better or worse. In general, we have less movement occurring thanks to covid, so the EU itslef has restricted that free movemtn of people that was the root of much of the anti-EU sentiment. Issues at the borders are being resolved at speed (almost impressively, actually) and the differnt border between Britain and NI is behaving well. Though we are all aware that a sporoportion of all companies have strucj a wait-and-see approach that means they, too, are sitting back and waiting to see what is what. Not least, what additional porcesses are incurred and what that takes (time, money, preparation, paperwork) and in consequence whether they will modify the business. Meaning to do business or not, as much as anythign else. Iam expecting us to adapt some of the covid resilience and simply recognise that some goods will become difficult (therefore change in price or availability) and so we'll simply swap them for somethign else. Already we can see that there are some businesses we will want to have onshore raher than shared. That will increase our independence, but it will also, I suspect,. coist us more. Right now the Bank and Gov't are printing money and oushing it in all directions; if we have to pay for this, we'll be largely bankrupt, so there seems to be anb assumption that monetary policy, even economic modelling principles, haev been rewritten. One hopes that this is not merely copying various collapsed economies such as the African states whose currencies broke.

[1] https://www.theweek.co.uk/brexit-0

[2] https://researchbriefings.parliament.uk/ResearchBriefing/Summary/CBP-7851 full report is a pdf.

Green-background diagrams from [2]

1 Financial services and other business services (a category which includes legal, accounting, advertising, research and development, architectural, engineering and other professional and technical services) are important categories of services exports to the EU – in 2017 these two service categories made up 52% of UK service exports to the EU. [2]