Much is written about social consequences and medical consequences but, amidst the clamour for lockdown to end, there is not very much coming to my attention about what follows in economic terms. Yes, the lockdown and crackdown is producing a recession, often defined as two successive quarters of reduced GDP ¹ But if we change "two successive quarters" to the less definite "lasting more than a few months", then I think we are already having a recession and reaching June still in lockdown (very likely) guarantees this. ² ³ ⁴

Recessions are not necessarily entirely bad things. They are characterised by business failures including banks and by increased unemployment. This can occur due to structural shifts in the economy as vulnerable or obsolete firms, industries, or technologies fail and are swept away; dramatic policy responses by government and monetary authorities, which can literally rewrite the rules for businesses; or social and political upheaval resulting from widespread unemployment and economic distress. We can now add to this last sentence the word pandemic.

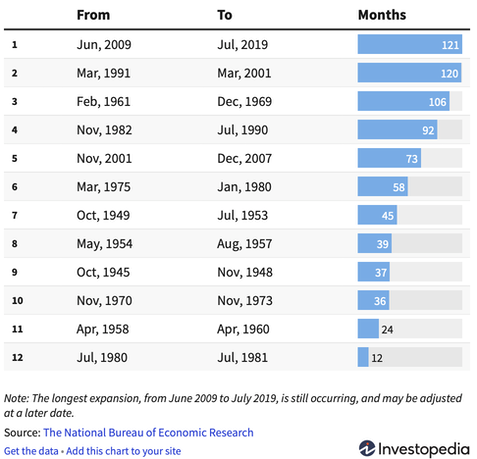

Recession is followed by recovery. Unsurprisingly the characteristics of recovery are the opposite of recession: growth of GDP, falling unemployment and a generally improved economy. So a renewal of sorts and entirely healthy, if somewhat uncomfortable. The chart to the right shows that they occur sufficiently often to be a factor in every business model, though having the ten years from 2009-19 entirely as expansion might excuse failure to do this.

One suspects that this time is a bit different, that we live in Interesting Times and are far from sure this is at all a Good Thing. Early indicators suggest households and businesses are facing the largest economic downturn in living memory; 70 per cent of households whose finances have been affected by coronavirus have experienced falls in income and a quarter of businesses have temporarily closed. But the Government’s economic support package, particularly the job retention scheme (JRS) appears to be successfully protecting families from very large fall in income, protecting many from additional hardship. This is reflected in consumer and business confidence which remain above financial crisis lows – although measures have fallen faster than they did in 2008/09. The Debt Management Office plans to tap the market for historically-large sums in the coming months to cover the massive increase in the Government’s cash requirements. Despite this, there is still no sign that financial markets are unable to digest the increase in borrowing. [2]

I wonder whether there is a connection between how hard the fall is and how long since the last recession. I've no idea how to quantify that but I leave it to you to investigate.

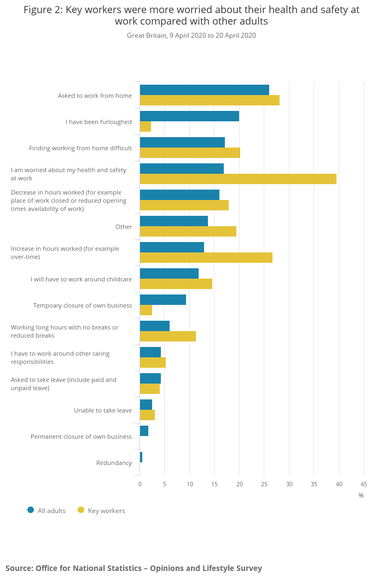

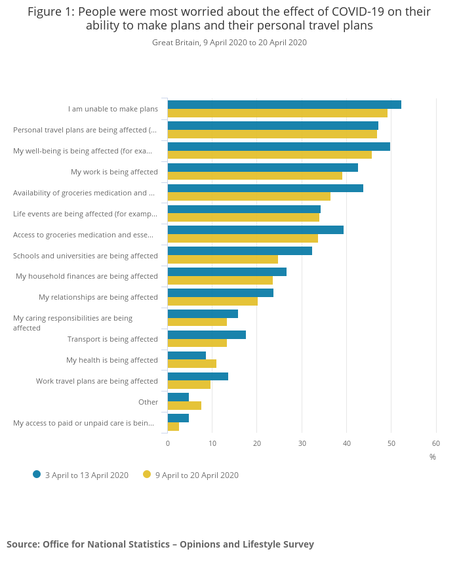

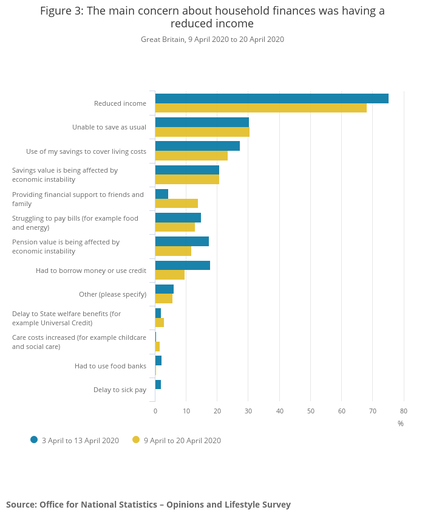

The Opinions and Lifestyle Survey (ONS) is easily found and is reported on in [6]. I have copied three Figures related to this survey, in colours that might be called blue/green and a dirty yellow. If you want to study them and draw conclusions for yourself, go to the site itself so as to read the notes. I've scaled them to fit my screen, not yours.

Staying at home [6] 30 April 2020

Over 8 in 10 adults (83.5%) said they had either not left their home or only left for one of the permitted reasons listed earlier in the past seven days, a similar level to last week (85.4%). This increased to 88.4% for those aged 70 years and over, and for those with an underlying health condition it was 85.7%.

Of the 16.5% who said they had left their home for something else, the main reason was to run errands.

There continued to be a high level of support for the Stay at home measures, with 84.0% of adults saying they strongly supported the measures and a further 12.5% saying they “tend to support” the measures.

Someone who is furloughed (for non-UK readers) at moment is paid 80% of their salary up to £30k per year direct from the state, but has not lost their job. This affects some 6.3 million people, 800 thousand businesses and that is about 20% of the working population. The ONS report [3] is hard work, not their fault but because the stats depend on businesses making responses. With that significant proviso, in the period 23Mar to 05Apr: 0.5% of the workforce has been made redundant, 5% was off sick or in isolation, 27% was furloughed and 76% of the work forces of the smaller group not fully trading was working as normal. Looking at that more closely (still confined by responses) only 3% of those in education have been furloughed, 6% in IT business but this is different where the businesses have temporarily ceased trading. I don't understand why these second figures are around 14% and not very much higher. Read the report for yourself; there are others. Takeaway message at 5th April (not 5th May) is that around a quarter of the workforce is furloughed and under 1% made redundant. Many of the sites I looked at return to sources [2] and [3], so I'll stick with them as primary. Yet I suspect that a lot of what is in [2] came from [3].

Q3 of that survey is relevant. The question was In which ways are your household finances being affected by the coronavirus (COVID-19)? Select all that apply. So if 74% declare a reduced income, does that mean that 26% have the same or an increased income? The responses to Q2, In which ways is your work being affected by the coronavirus (COVID-19)? included around 27% key-workers (and 13% of all) reporting increased hours with half of those numbers declaring that the lack of breaks is an issue. Read [5] and [6], please.

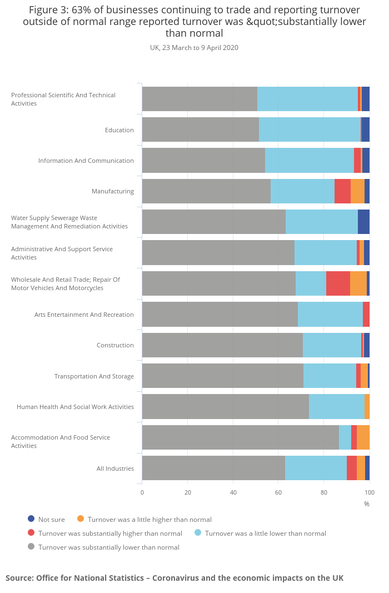

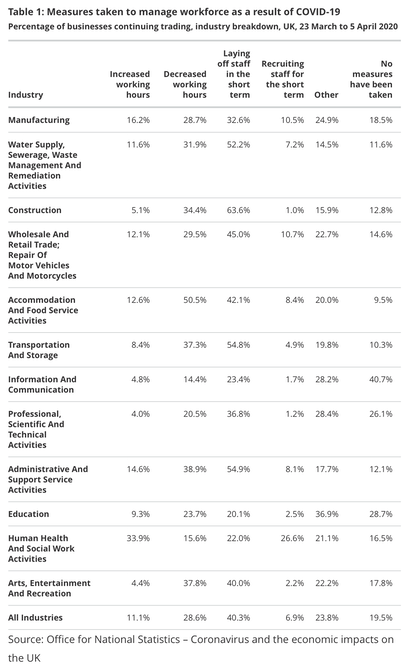

Table 1, from [4] shows that the picture is complicated. So much so that I don't think any conclusions can be drawn without confining one's comments to something specific such as one of these classes of industry.

I don't feel to be succeeding in exploring what the economic consequences are. Public debt has obviously soared to levels we haven't seen before. We have seen shocks to the supply system, exemplified by the loss of supply from China when they were shut down, and to the demand side of the economy as consumers are confined to their houses and businesses struggle to survive at all. So consumer spending has moved quite dramatically, which will cause some businesses to fail. Government response has been to attempt to shore up against these failures and we will see whether that has any positive effects later, perhaps next year in the inevitable recovery. But, as the initial description of recession says, renewal is expected and that rather implies change. We already are anticipating dramatic change to the travel industry, exemplified by the staff reduction in airlines and, as it seems more likely that crowding together will be discouraged for a long time (more like a year than the odd additional month), so much of the hospitality industry will stay severely depressed. So will many leisure activities, notably sport and religion. ² [7]

DJS 20200505

1 The NBER defines a recession as a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales. [1]

2 I noticed with amusement a question at the Downing Street briefing yesterday, which addressed the restriction of religion but decried the multiple mentions of sport. What made me grin was that it was obvious to me that the minister was dying to say that these are the same (in the context of mass meetings where close contact is expected), but simultaneously recognising that this would be grossly misunderstood as a Wrong statement. Such is the PC position we are in. Yet there are many ways in which football DOES qualify as a religion and I've said so for years. Discuss as an essay topic. I'll leave further exploration to you. Oh look, some have already responded: http://theindependent.sg/pray-tell-me-is-football-a-religion/, https://bleacherreport.com/articles/59738-the-cultof-football-a-religion-for-the-twentieth-century-and-beyond, https://www.theguardian.com/commentisfree/2013/sep/02/why-football-doesnt-measure-up. The third of these argues that football largely excludes women and that it lacks theology. Argue with those two ideas, please.

[1] https://www.investopedia.com/terms/r/recession.asp

[2] https://www.resolutionfoundation.org/publications/the-economic-effects-of-coronavirus-in-the-uk/ Please be aware that this is updated weekly. Later edit: I found one labelled 'final' and dated 14th May, so that is where you'll be pointed by the link. No doubt you will treat this as modern history.

[7] https://commonslibrary.parliament.uk/research-briefings/cbp-8866/

Related pages:

Essay 291 - Effects of an outbreak what it says, effects, but some description of what we have (and not)

Essay 293 - Covid-19 charts

Coronavirus (Y10+) modelling problems

Epidemics more general theory

Infectious disease looking at the 2020 problem, particularly effects of the reproduction number changing.

Viruses are very small

Essay 318 Covid in October Charts updated through November

Essay 322 Covid in November UK Regional chart and table through Lockdown Two

Essay 325 Covid in December Updated graphs of rate and prevalence, plus US charts.

Essay 328 Vaccine progress What it says on the tin.

Essay 332 Covid in January Lockdown 3 takes effect

Essay 337 Covid in February This very page.